Considerations for Interest Rate Risk Modeling in an Elevated Rate Environment

by Adam Krueger, Banking Analyst I, Supervision and Regulation, Federal Reserve Bank of Cleveland

Interest rates have effectively been at or near zero for most of the past 15 years, resulting in a relatively stable rate environment. However, with inflation rates in 2022 reaching the highest level since the early 1980s, the Federal Open Market Committee increased the federal funds target rate for the first time since 2018.1 This began the most rapid rate hike in four decades. As of September 20, 2023, the target rate had increased by 525 basis points. As a result of the increases, many community bankers are grappling with new balance sheet management strategies because unrealized losses have quickly crept into investment and loan portfolios, while deposit and borrowing costs have been rising.

These rate hikes have directly impacted community banking organizations (CBOs), which have largely been flush with deposits since the COVID-19 pandemic. As costs stayed low and depositors held their funds in banks in the face of uncertainty, deposits represented a relatively stable source of funding. Banks with assets that repriced faster than funding benefited from rising interest rates; however, some banks with rate-sensitive funding or longer-term assets have had net interest margins compress. Rising rate environments can also put a strain on the ability of banks to maintain access to stable funding sources, especially when low-cost deposits begin to run off as depositors seek higher-rate alternatives. Investment portfolios, long understood to be a consistent source of asset-based liquidity for CBOs, have suffered from accumulating unrealized losses, hampering the ability of some banks to fund these deposit outflows.

The elevated rate environment and uncertain outlook have fundamentally changed banks’ risk profiles and funds management practices. Therefore, supervisors are stressing the importance of sound interest rate risk (IRR) management. This article provides an overview of effective IRR management practices and additional modeling considerations for bankers.

A Brief Overview of Interest Rate Risk

IRR is the potential that changes in interest rates will adversely affect cash flows or the value of assets or liabilities. IRR is inherent in all balance sheets and is a primary risk (along with credit risk and liquidity risk) associated with traditional banking practices. At most safety and soundness examinations, IRR is the key factor that examiners consider when evaluating a bank’s “Sensitivity to Market Risk,” which is the “S” component of the supervisory CAMELS rating framework.2 Whether a CBO engages a vendor to measure IRR or conducts the modeling in-house, IRR management is heavily reliant on quantitative models. Typical CBOs measure IRR using the tools described in the table:3

Table: Common Types of IRR Measurement Systems

|

Measurement Tool |

What It Measures |

Calculation |

|

Gap Analysis |

Comparison of the amount of rate-sensitive assets (RSAs) and the level of rate-sensitive liabilities (RSLs) over given time bands. The difference represents the amount of assets exposed to IRR, with a negative value representing a liability sensitivity to rates. Gap analysis is often used by banks to get a general understanding of repricing risks over time, but it treats all RSAs and RSLs equally and will likely not satisfy regulatory expectations on its own. |

RSA – RSL = Gap |

|

Earnings at Risk |

Income simulation under various interest rate scenarios to estimate the effect of potential rate changes on net interest income (NII) as assets and liabilities reprice over a given time frame, typically up to two years. Reduced earnings or losses could adversely impact capital and liquidity positions. |

Change in NII/Base Case NII |

|

Economic Value of Equity (EVE) |

Simulation under various interest rate scenarios measuring the effect that rate changes have on the discounted value of all future expected cash flows and the value of capital generated by a bank’s current financial position. This approach focuses on a longer-term time horizon. Adverse outputs could signal future earnings and capital problems. |

(Change in Economic Value of Assets – Change in Economic Value of Liabilities)/Base EVE* |

Source: The Commercial Bank Examination Manual, Section 3300.1: Interest Rate Risk Management. *Note: The denominator can vary depending on different EVE modeling providers; however, it is usually some measure of capital (e.g., tier 1 capital).

Revisiting IRR Guidance

Although it is bank management’s role to be informed — but not to speculate — on the likely path of interest rates, the Federal Reserve, along with other regulatory agencies, has issued guidance on IRR management to help manage risk against both expected and unexpected changes in rates in any rate environment. However, given the recent rapid increases in interest rates and the changing macroeconomic landscape, this guidance has become more important for banks to consider in maintaining safe and sound practices. The guidance is set forth through Supervision and Regulation (SR) letters 96-13,4 10-1,5 11-7,6 and 12-27 (referred to collectively as “interagency guidance”), which lay out the main pillars of IRR management through effective corporate governance and model risk management.

Corporate Governance

Sound IRR management begins with appropriate policies, procedures, and controls set by the bank’s board of directors and senior management. To monitor risk exposures and compliance with risk tolerances, there should be a comprehensive set of systems and standards for measuring a bank’s IRR.

The crux of a community bank’s IRR measurement system is its internal stress testing, which primarily includes EVE and earnings at risk models. The Commercial Bank Examination Manual explains an approach that a bank might take in its IRR modeling, such as incorporating 100 and 200 basis point parallel shocks, and also suggests banks consider using rates of greater magnitude, such as plus or minus 300 and 400 basis point shocks. Banks should also model scenarios involving prolonged rate shocks; shocks that address the bank’s key basis risks, such as mortgage spreads; and different yield curve scenarios involving nonparallel changes to different tenors on the yield curve. Dynamic modeling can also be effective in planning for future market risk, especially for a bank with strategic plans to grow or shrink its balance sheet or change its composition. However, dynamic modeling is not a replacement for static balance sheet modeling, as increased reliance on dynamic outputs can mask current exposures.

Appropriately justified bank-specific assumptions are critical aspects of effective IRR management. Assumption methodologies should be consistent with the size and complexity of the bank, but in any case, they must be understood by management and supportable. These include assumptions regarding asset prepayment speeds, nonmaturity deposit decay rates (the percentage of deposits expected to run off the balance sheet over a given period), and deposit betas (the percentage of market rate changes passed along to depositors). Senior management should also stress test these assumptions by assessing the impact that different assumption values would have on the bank’s model outputs and risk exposure. As a safe and sound practice, management can compare these stress test results to preestablished tolerance limits.8

IRR Model Risk Management

Because IRR management broadly relies on model results, banks incur inherent model risk, which is the potential for adverse consequences from decisions that are based on incorrect or misused model outputs and reports. The inherent risks in using models to measure IRR can typically be controlled through model risk management practices.9 Internal controls and validation processes surrounding IRR modeling are key to ensuring that model outputs are accurate. There are three main pillars of effective model validation: (1) evaluation of conceptual soundness, (2) ongoing monitoring, and (3) outcomes analysis.

- Conceptual soundness is a core determinant of an IRR model’s accuracy. A verification of conceptual soundness will ensure that the model has a reasonable development process, including independent testing of its theoretical and mathematical soundness. This should include empirical evidence for the methods used and variables selected, and documentation should convey to the model user any of the model’s limitations and any assumptions that may impact the model’s performance. Many CBOs opt to use vendor-supplied models to measure IRR. A CBO that does this should still employ sound risk management practices in IRR model risk governance and incorporate the vendor’s IRR model into its broader risk management framework. However, a CBO can rely on testing performed by model validators commissioned by the vendor as long as the validation is independent, tests the mechanics and mathematics, and provides clients with appropriate testing results and limitations. A bank relying solely on written confirmation that the vendor’s model has been validated will likely not satisfy supervisory expectations.10

- The second pillar of effective IRR model validation includes a program of ongoing monitoring and evaluation of model performance along with a system for responding to noted variances. This would include checks, controls, and procedures to ensure that all aspects of the model are accurate and functioning as intended, particularly for user-developed applications such as spreadsheets. The audit function should assess the overall model risk management framework, and internal auditors should ensure that the validation activities are being performed accurately and within acceptable time frames and that the operational systems and data used by the models are reliable.

- Finally, outcomes analysis can help a bank determine whether models are functioning as intended by comparing model outputs with corresponding actual outcomes. In addition to simple backtesting, interagency guidance has encouraged the use of “early warning” metrics to be compared with preestablished limits to benchmark model accuracy, as backtesting results could reveal inadequacies too late. This risk is particularly present after the introduction of a new model.

Considerations for a Post–Rate Shock Environment

Prudent IRR management involves regular assessment of the adequacy of model assumptions, inputs, and associated outputs. It could also include reevaluating IRR modeling practices in a post–rate shock environment, changing the strategic plan, analyzing the broader macroeconomic environment, and considering any identified potential data or assumption limitations. Given the recent shift in the interest rate landscape, banks may experience changes in operational strategy, new patterns of customer behavior, and opportunities to challenge the soundness of their modeling inputs and scenario analysis.

Changes in Strategic Plans

Before the 2022–2023 rate tightening cycle, some CBOs adjusted their operating strategies to combat earnings pressures and deploy excess funding accumulated on balance sheets. For example, many banks adjusted their investing strategies and increased the size of their securities portfolios. Any time a bank’s balance sheet management strategies change, it is important that management and the board of directors are sufficiently informed about the associated risks. IRR reporting should be used to assess how the new balance sheet structures change the risk profile of the bank before management makes material pivots in strategy. Sound risk management practices should also consider possible changes to a bank’s deposit base, including how depositors will react to shifts in the macroeconomic environment. SR letter 12-2 notes that management should carefully consider how customer behavior may change during periods of stress as well as the external factors that may influence that behavior. When analyzing possible future deposit flows, banks should identify the types of market shocks that would influence depositor behavior to ensure that deposit concentration risk is well understood and managed.11 This prospective analysis will impact important IRR model assumptions, such as deposit decay rates and deposit betas.

Nonmaturity Deposit Decay Rates

Nonmaturity deposit (NMD) decay rates reflect how “sticky” a bank’s NMDs are. These assumptions help management match cash flows and understand how quickly the bank would need to replace deposits under different interest rate scenarios. Developing an understanding of the bank’s deposit base includes assessing how deposit decay rates will differ between types of client accounts. For example, corporate depositors with larger balances may be more sensitive to interest rates and react more dramatically to rate shocks than other depositors. If a bank has increased exposure to these more rate-sensitive depositors since the last time assumptions were developed, the decay rates used in the model would be worth revisiting. Another specific example noted in SR letter 12-2 is the impact of stress on consumer deposit behavior, including a shift toward insured deposits that may impact NMD decay rates. Even if a depositor has had a long-term relationship with a bank, the relationship coinciding with a steady rate environment may mask how the depositor will react when rates change. SR letter 12-2 also mentions the potential impact on time deposit decay rates as rates rise in addition to NMD decay rates.

Deposit Betas

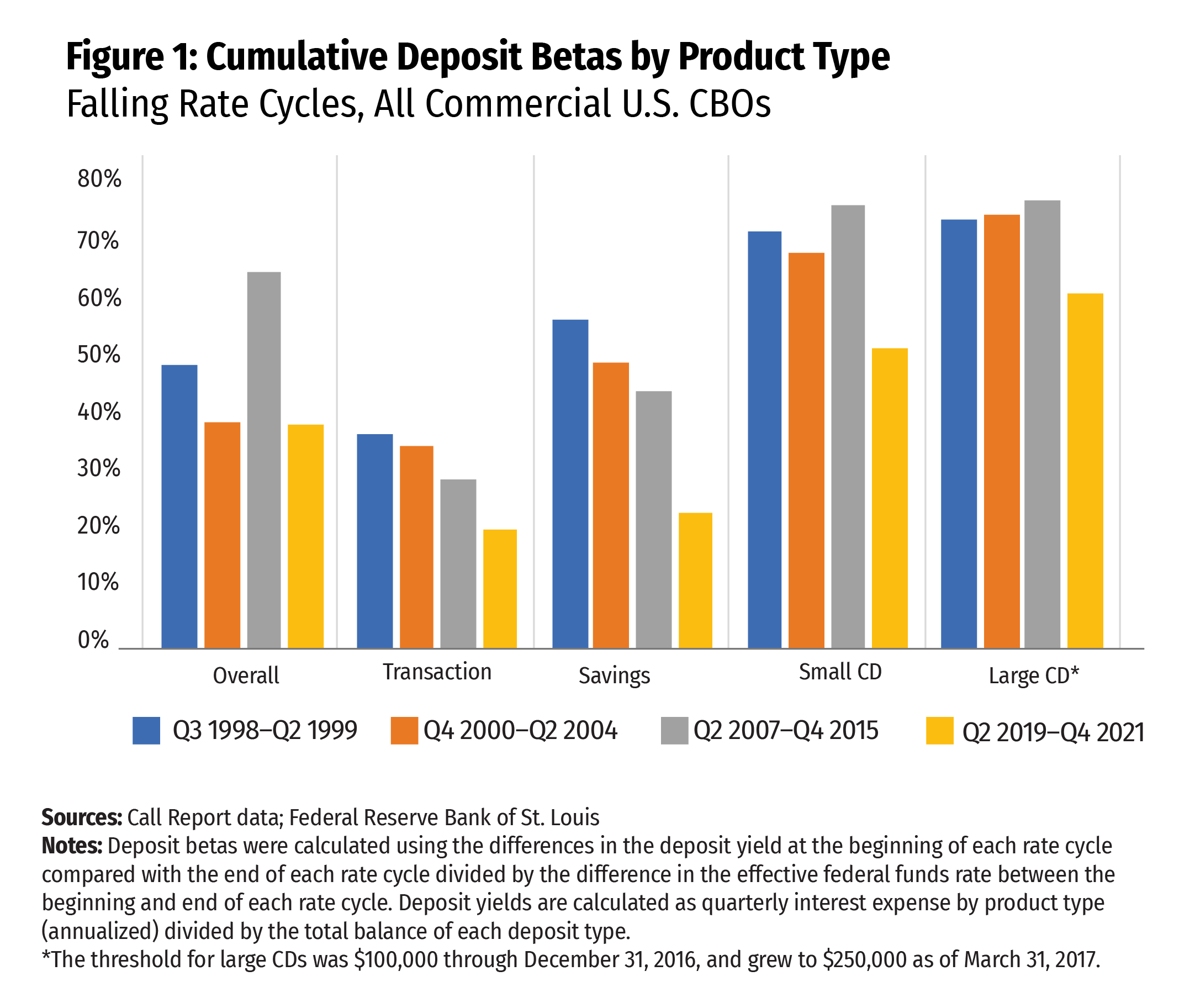

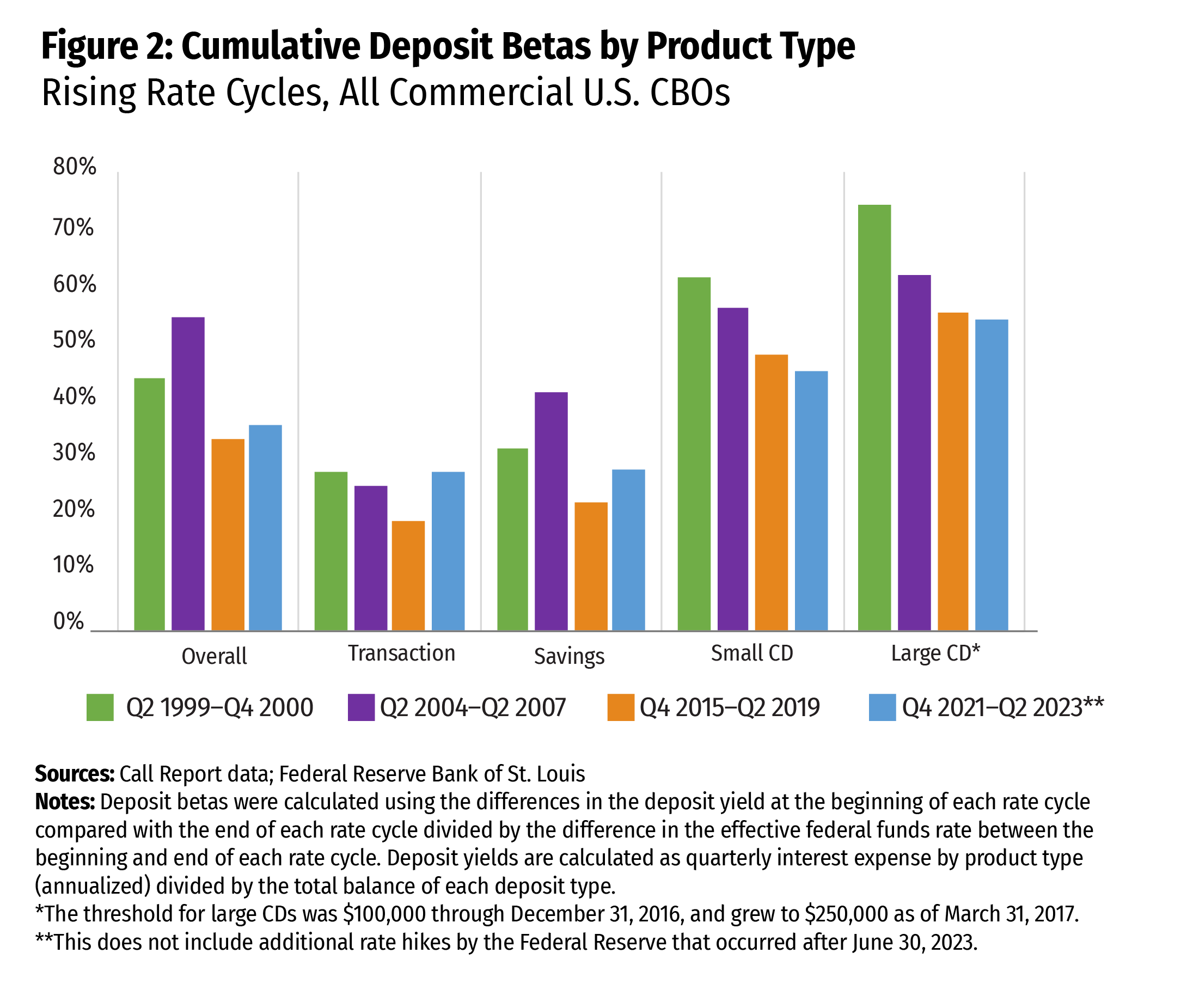

This rate cycle has been an opportunity for banks to revisit deposit beta assumptions and ensure their reasonableness. Much like NMD decay assumptions, deposit betas largely depend on both the composition of a bank’s deposit base and the types of deposit products that the bank offers. While sound IRR management practices would already include projecting deposit betas by product type, it may also be beneficial to think about different deposit betas by the size of the deposit and by the different types of customers (see Figures 1 and 2 for the author’s estimates on cumulative deposit betas by deposit type for four recent falling and four recent rising rate cycles across community banks).

A bank should also consider the composition of deposits across its public, corporate, and consumer (retail) customers. Academic research shows that the beta of a specific product type that includes uninsured deposits should, in theory, have a value closer to 1 than the beta for the same product type that is fully insured.12 Thus, uninsured deposits should be modeled with a shorter duration. A higher share of uninsured deposits could result in a higher overall deposit beta; lower assumed deposit betas for uninsured deposits could result in the underestimation of a bank’s exposure, especially for banks with high concentrations of large depositors. Before 2012, uninsured deposits were primarily in large certificates of deposit (CDs); however, this balance then shifted over to checking and savings accounts, which generally have lower deposit betas. The assumption that account type, rather than access to deposit insurance, impacts rate sensitivity could result in an increased risk of underestimating deposit betas (and deposit decay rates), as uninsured depositors may behave differently than insured depositors, particularly in times of volatility.

Market interest rates have remained well above the zero lower bound since March 2022, and bankers are now left to consider how assumptions will hold up in both positive and negative rate shock environments. One area that could be revisited is how deposit betas have performed to date, with the results used to help develop assumptions in a downward rate shock. If a bank had to raise deposit costs at amounts that came in below deposit beta expectations, it should ensure that deposit betas in a falling rate scenario are still commensurate with their ability to reduce rates without falling below zero. Deposit rates can effectively only come down as much as they have increased if they began near zero. An overstatement of deposit betas in a downward shock could result in inaccurate model outputs that would show the bank to be in a more liability sensitive position than it truly is.

Deposit betas can be asymmetric, meaning that banks may be able to reduce the interest rates paid on deposits in a falling rate environment at a faster pace than they would have to increase the rates paid on deposits in a rising rate environment. This notion is generally demonstrated in Figures 1 and 2. Some research suggests that there is limited evidence that asymmetries exist for deposit betas.13 However, other evidence shows that banks are faster to adjust deposit rates downward only in short-term scenarios; this does not apply in a time frame of over one year or for cumulative deposit betas.14 A CBO’s deposit beta will largely depend on its market pricing power. If a bank exhibits higher local pricing power in its respective market, its ability to act as a price maker increases, allowing it to manage interest expenses more favorably. Each CBO should consider its own respective deposit base, market competition, and economic environment when developing assumptions. Interagency guidance reminds bankers that using industrywide or generic model assumptions is generally not consistent with effective risk management practices.

Other Model Implementation Considerations

Bank management and the board of directors should assess potential limitations within the bank’s current modeling capabilities, including an assessment of embedded assumptions, ranges of input values, or market conditions. This would include assumption stress testing, which was discussed previously in this article. Banks using a third-party vendor’s model can learn more about the model’s limitations through active engagement with the vendor. If limitations do exist, sound risk management could involve monitoring certain inputs and market conditions through early warning signals. For example, if a model is reliant on the assumption of a normal yield curve, operating in an environment with an inverted yield curve could result in inaccurate projections of future cash flows or the value of the bank’s equity. Additional consideration may be given to the differences in customer behavior during prolonged rate shocks and brief adjustments in market rates, as well as to the longevity of model assumptions.

A post–rate shock environment also provides management with an opportunity to test the bank’s model assumptions and model outputs. After a rate shock, backtesting allows management to verify whether the bank’s internal or outsourced model is working as expected and if assumptions are still supportable. It is important for bank management to critically evaluate these factors, which could significantly impact strategic decision-making going forward.

Conclusion

A post–rate shock environment poses both unique risks and opportunities for CBO management. Appropriate corporate governance and model risk management are vital aspects of sound IRR management. The main tenets of existing interagency guidance apply to any economic environment; however, a changing operational environment or a change to the risk profile of a bank could warrant the adjustment of risk management practices. The most recent rate shock can be used as a benchmark for banks to assess the adequacy of their policies and procedures and to identify any opportunities for improvement, including an assessment of current model risk management practices. As the current environment has highlighted, it is important that management teams continue to proactively reevaluate their risk management practices, identifying the potential risks on the horizon and adequately aligning bank strategy to address those risks.

- 1 See Sarah Foster, “Fed’s Interest Rate History: The Federal Funds Rate from 1981 to the Present,” Bankrate, March 20, 2024, available at www.bankrate.com/banking/federal-reserve/history-of-federal-funds-rate/#2021.

- 2 See the Commercial Bank Examination Manual, Section 3300.1: Interest Rate Risk Management, available at www.federalreserve.gov/publications/files/cbem-3000-202310.pdf.

- 3 For more information on CBO IRR, see Emily Greenwald and Doug Gray, “Essentials of Effective Interest Rate Risk Measurement,” Community Banking Connections, Third Quarter 2013, available at www.cbcfrs.org/articles/2013/q3/essentials-of-effective-interest-rate-risk-measurement.

- 4 See SR letter 96-13, “Joint Policy Statement on Interest Rate Risk,” available at www.federalreserve.gov/boarddocs/srletters/1996/sr9613.htm.

- 5 See SR letter 10-1, “Interagency Advisory on Interest Rate Risk,” available at www.federalreserve.gov/boarddocs/srletters/2010/sr1001.htm.

- 6 See SR letter 11-7, “Guidance on Model Risk Management,” available at www.federalreserve.gov/supervisionreg/srletters/sr1107.htm.

- 7 See SR letter 12-2, “Questions and Answers on Interagency Advisory on Interest Rate Risk Management,” available at www.federalreserve.gov/supervisionreg/srletters/sr1202.htm.

- 8 For more information on effective corporate governance, see Doug Gray, “Effective Asset/Liability Management: A View from the Top,” Community Banking Connections, First Quarter 2013, available at www.cbcfrs.org/articles/2013/Q1/Effective-Asset-Liability-Management, and Emily Greenwald and Doug Gray, “Essentials of Effective Interest Rate Risk Measurement,” Community Banking Connections, Third Quarter 2013.

- 9 See SR letter 11-7.

- 10 See SR letter 12-2.

- 11 See Commercial Bank Examination Manual, Section 3000 — Capital, Earnings, Liquidity, and Sensitivity to Market Risk.

- 12 See Itamar Drechsler, Alexi Savov, Philipp Schnabl, and Olivier Wang, “Banking on Uninsured Deposits,” NBER Working Paper Series, Revised June 2023, available at www.nber.org/system/files/working_papers/w31138/w31138.pdf.

- 13 See Jeffrey R. Gerlach, Nada Mora, and Pinar Uysal, “Bank Funding Costs in a Rising Interest Rate Environment,” Journal of Banking & Finance, 87 (February 2018), pp. 164–186, available at www.sciencedirect.com/science/article/pii/S0378426617302248.

- 14 See Itamar Drechsler, Alexi Savov, and Philipp Schnabl, “Banking on Deposits: Maturity Transformation Without Interest Rate Risk,” Journal of Finance, 76:3 (2021), pp. 1091–1143, available at https://pages.stern.nyu.edu/~asavov/alexisavov/Alexi_Savov_files/BankingOnDeposits.pdf.