View from the District: Deposits in a Digital World

by Emily Greenwald, Senior Vice President — Head of Banking Supervision and Regulation, Credit, Risk, and Reserves Management, Federal Reserve Bank of Dallas

I remember opening my first savings account at Dupont State Bank in Dupont, IN. I was five years old and handed over the cash I had earned from working with the livestock on my family’s farm. In return, I received a book in which the bank teller had neatly handwritten my account information, including the amount I had deposited. The two tellers greeted me by name as I walked in the door and waved as we said goodbye. After all, in a town of fewer than 300 people, everyone knew everyone. I would go on to excitedly add entries to my book as I grew older. Gradually, the savings book collected dust, tucked away in an old tin can on my bedroom shelf that also contained such valuable items as a collection of interesting buttons and a silver dollar. Occasionally, I would open the book to look at the money that I knew was safely tucked away in my community bank.

Community banks have long prided themselves on knowing their customers and the communities that they serve. The Eleventh District is an excellent example of these strong ties. Texas, where I live today, is home to the largest number of community banks in the nation. There are over 400 community banks supporting communities in the Lone Star State.1 Techniques honed by years of community investment and a focus on customer service are hallmarks of the strong community banking organizations (CBOs) we engage with today. Yet, the deposit world in which community banks now operate is far different than it was in the days of physical passbook savings accounts. The foot traffic patterns of brick-and-mortar businesses have changed. Accounts can now be opened and closed electronically. Depositors, once assumed to be “sticky,” can — and have — moved funds in response to interest rate arbitrage and social media trends.

Challenging Norms

Many community banks weathered the liquidity challenges in March 2023 with ease, even gaining market share in some regions. However, community banks are not immune to the rapid technology-enabled changes impacting our economy. One wonders how George Bailey of It’s a Wonderful Life could have inspired his customers to remain calm and committed had the run on his bank originated on TikTok.2

The modern deposit world presents an opportunity for community bankers to enhance their asset liability management and challenge long-held norms in their funding and interest rate risk practices. In this article, I highlight three simple risk management plans that community banks can employ to enhance their understanding of deposits and prepare for funding risks: (1) planning for continued deposit competition, (2) planning to measure deposits differently, and (3) planning for on-the-ready contingent funding sources, such as the Federal Reserve’s discount window. These practices can supplement existing deposit-gathering and retention techniques.

Plan for (Continued) Fierce Deposit Competition

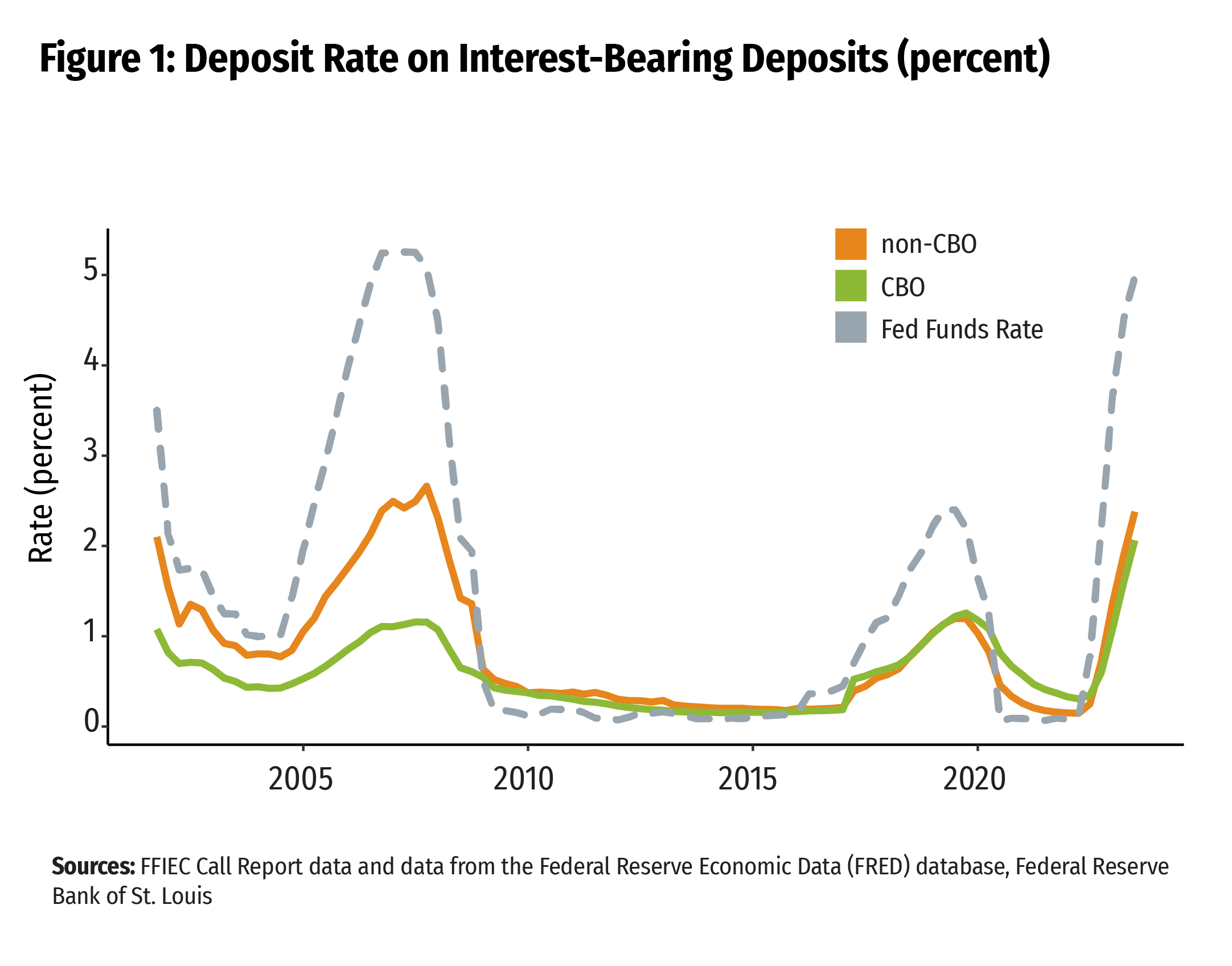

Historically, community banks have enjoyed low-cost deposit products. However, we have heard anecdotally in the Eleventh District that competition for deposit products is driving up the cost of funds at all institutions, including community banks. I asked my team to look at the performance of bank deposit rates — both in the Eleventh District and nationally — during interest rate cycles from the past 20 years, and two interesting observations are noteworthy. First, the deposit rates of CBOs seem to be rising almost as quickly as non-CBO deposit rates in the current rate cycle (see Figure 1). Second, across all banks, deposit betas3 appear higher than they have in the past.

A decade ago, I wrote about the need for community banks to sensitivity test their deposit assumptions4 — that is, to take current assumptions and dramatically alter one to see the impact on the overall results. Sensitivity testing remains a useful tool for community banks to challenge long-held deposit views and to see the range of possibilities that interest rate risk modeling and cash flow projections produce. This is particularly important in the current landscape, as competition for deposits has intensified.

In addition, many basic interest rate risk models measure deposit betas linearly via a single deposit beta for all rate changes. Dynamic deposit betas that increase, particularly as market rate movements get larger, can effectively estimate the deposit competition that can occur as customers demand more interest for holding their funds.5

Plan to Measure and Test Deposits Differently

Since deposits comprise such a material volume of a bank’s liabilities, the characteristics of deposits are important to understand. Looking at how deposits are dimensioned and how the deposit mix may shift can aid in identifying risk.

Today’s deposits require going beyond size and product type to think about what other deposit characteristics should be considered. Measuring and monitoring deposits by different traits is becoming a more valuable part of ongoing liquidity and interest rate risk management. Traits beyond deposit size, age, and product type may provide valuable insights for senior management and boards of directors on how to better target retention marketing campaigns and vulnerabilities.

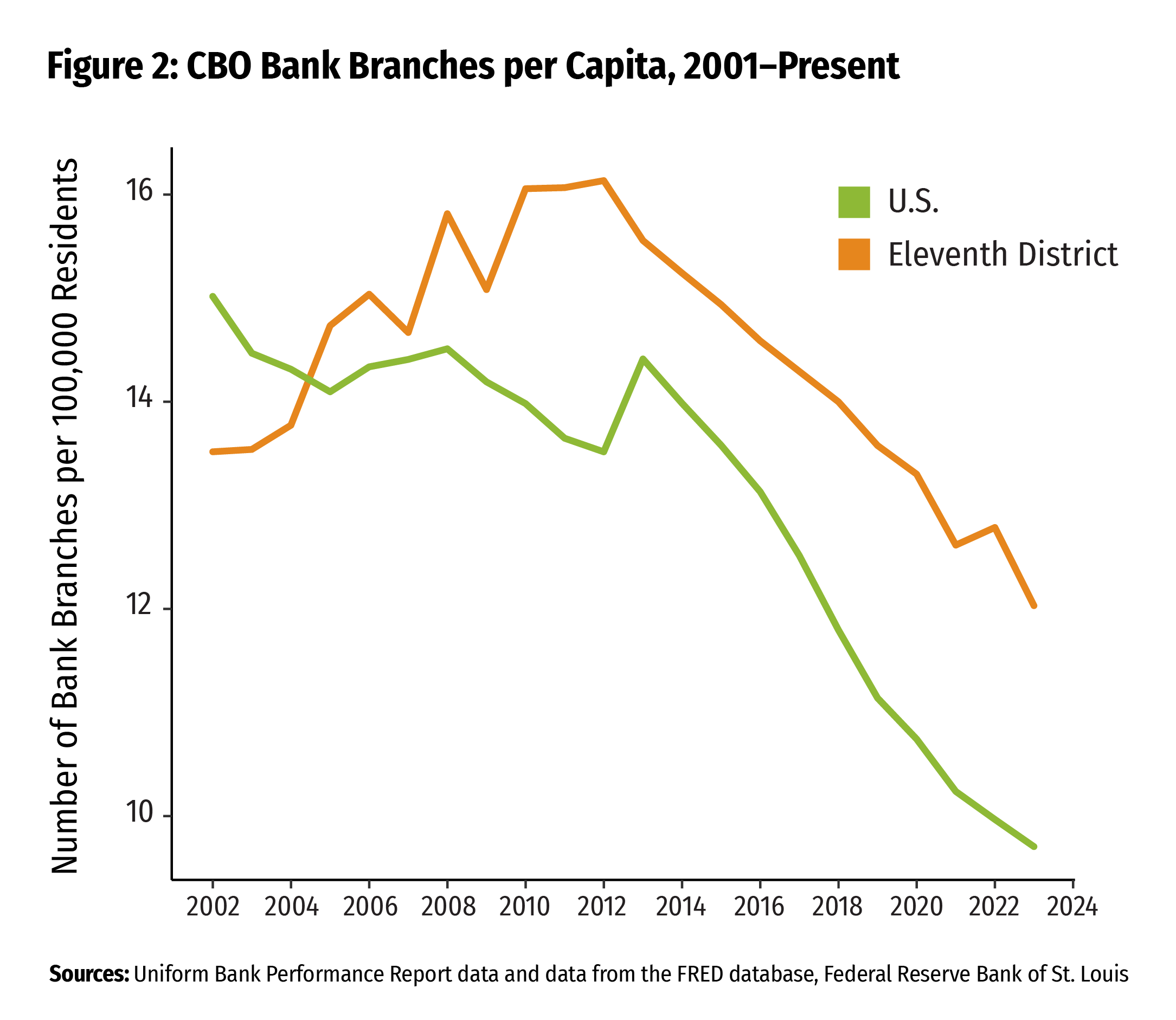

Let’s illustrate this point by looking at how deposits are sourced. As seen in Figure 2, CBO branches peaked at almost 16 per 100,000 adults in the United States in 2009 and have steadily declined thereafter, even in the Eleventh District, where branch activity performs above the national average. This trend is not necessarily surprising given customer sentiments on technology and banking. A Federal Deposit Insurance Corporation (FDIC) survey found similar results, with mobile banking usage sharply increasing from 2017 to 2021.6

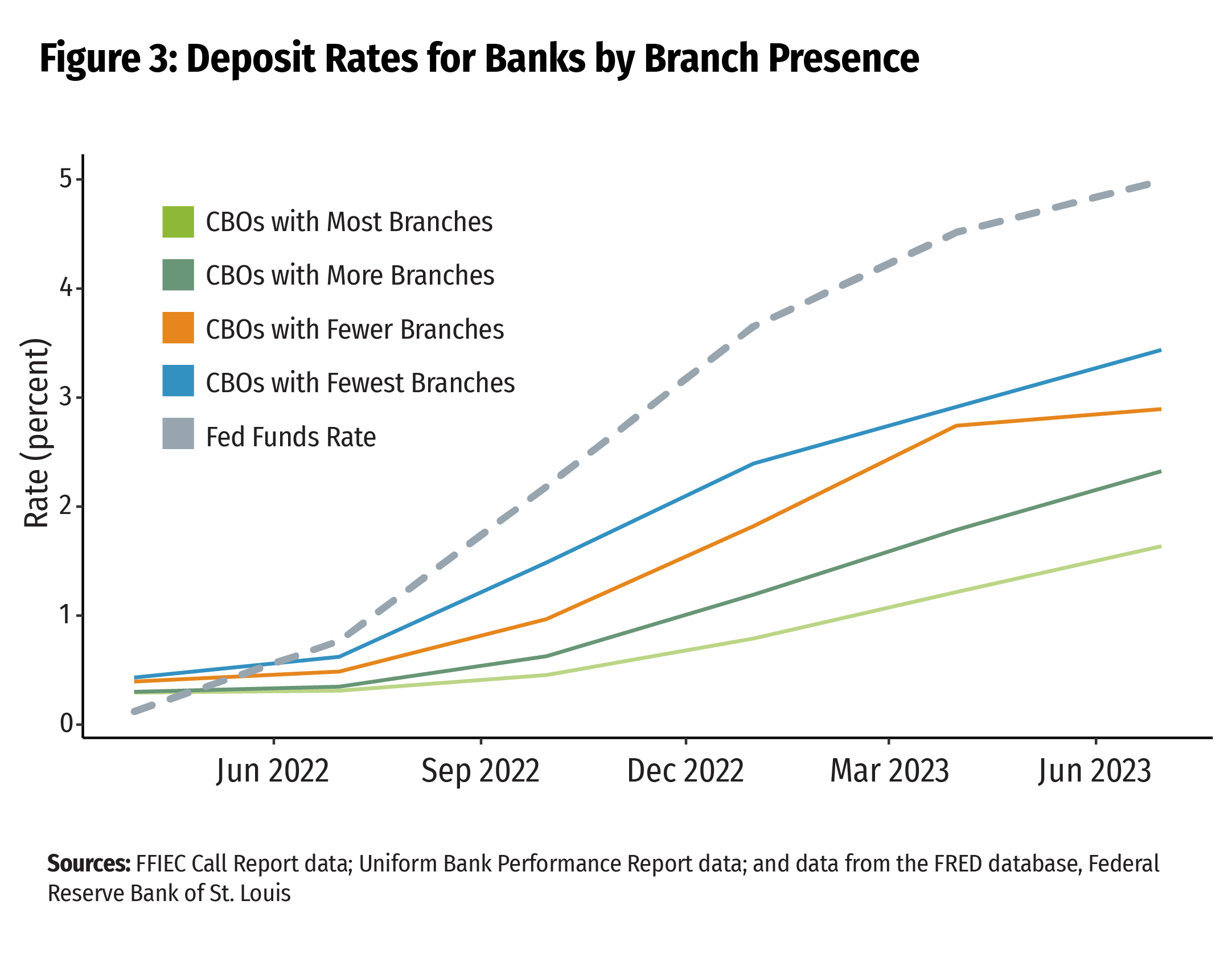

Branch- or internet-generated deposits may have attributes beyond deposit product type that are worth exploring in a dimensioning exercise. To explore the effect that these traits may have on an institution, Figure 3 groups CBOs nationwide by value of deposits per bank branch, which can serve as an approximate measure of the level of internet-based business. For simplicity, we assume that banks with fewer branches source more of their deposit gathering through the internet. We can see that CBOs with more branches to service their deposits (light green) have raised deposit rates more gradually than CBOs with fewer branches.7 Put differently, banks that have gotten deposits without the branch relationship — those that, in theory, may rely more on internet gathering — are finding that customers need to be paid more to stay. These customers may be more rate sensitive than customers whose loyalty has been gained through in-person relationships.

Thinking through the overarching behavior and intentions of customers depositing money online can better equip community banks as the deposit landscape continues to be reshaped by technology. Deposit dimensioning can also help in identifying other traits that may be material to a particular organization. For instance, banks can better identify deposit concentrations that may arise from a particular industry or business. Because deposits can now move faster, it is helpful for banks to know these dimensions when targeted outreach campaigns are needed for retention or to better track and prepare for the liquidity interruptions that may occur.

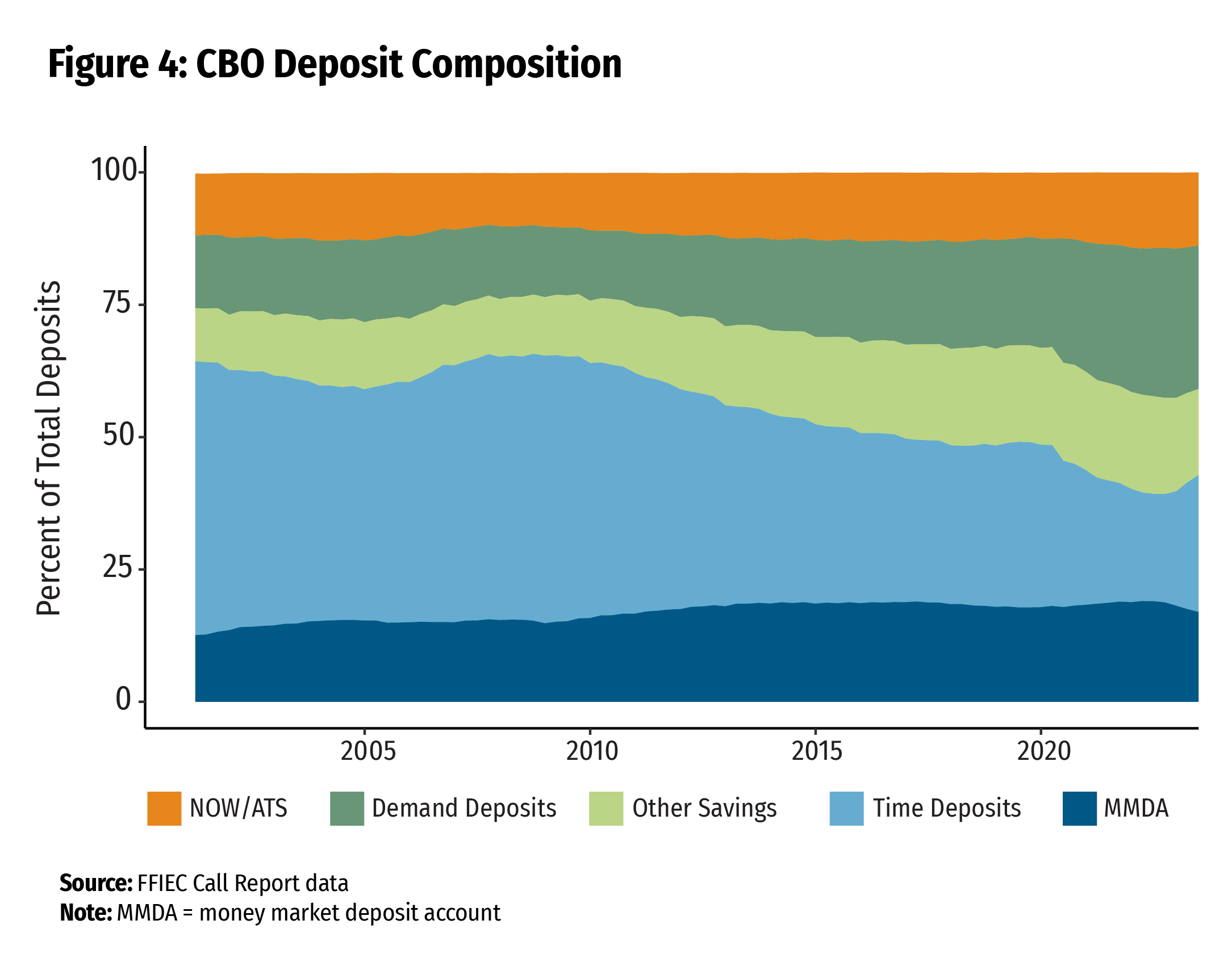

Measuring and planning for shifts in the mix of deposits can be another way to identify potential risks. Looking at deposit composition over different rate cycles, the mix of deposits at community banks changes (see Figure 4). Time deposits accounted for 52 percent of CBO deposits in 2001, but they made up only about half of that, 26 percent of CBO deposits, in 2023. Overall, savings accounts fell from 74 percent of CBO deposits to only 59 percent between 2001 and 2023, meaning that operational/transactional demand deposits and negotiable order of withdrawal/automatic transfer service (NOW/ATS) accounts have become a larger part of community bank funding. This was particularly true as market rates remained low for an extended period.

Periodically measuring and reporting on how the deposit mix may change, including reverting to greater time deposit representation, can help identify interest rate risk and liquidity risks that could occur if depositors choose different products over time.

Plan for On-the-Ready Contingent Funding Sources, Including the Fed’s Discount Window

Importantly, the speed at which deposits can move makes contingency funding critical for institutions of all sizes. Contingency funding readiness includes securing contingent funding sources, pledging collateral if needed, and testing these relationships. Each of these three actions is important for liquidity risk management.

The Federal Reserve discount window is an essential contingency funding tool that can be vital in a period of liquidity stress. Within the Eleventh District, over 75 percent of the banks8 have established discount window access. Lorie Logan, president and CEO of the Federal Reserve Bank of Dallas, has encouraged all banks within the Eleventh District to be prepared to access the discount window for operational resilience.9 I share her views.

Setting up access to the discount window is free, yet some banks remain reluctant to sign up. Contacts I’ve heard from during industry outreach events in Texas, New Mexico, and Louisiana cite the stigma associated with the perception of “needing” access to the discount window as the biggest barrier to establishing access. Historically, the discount window fell out of favor in the 1920s, and restrictions were placed on bank borrowings, including requirements of proof that all other funding sources had been exhausted.10 Such requirements led to assumptions that only troubled banks would borrow from the discount window, and these assumptions persisted until reforms that were put in place in 200311 aimed to remove any stigma from the use of the discount window.

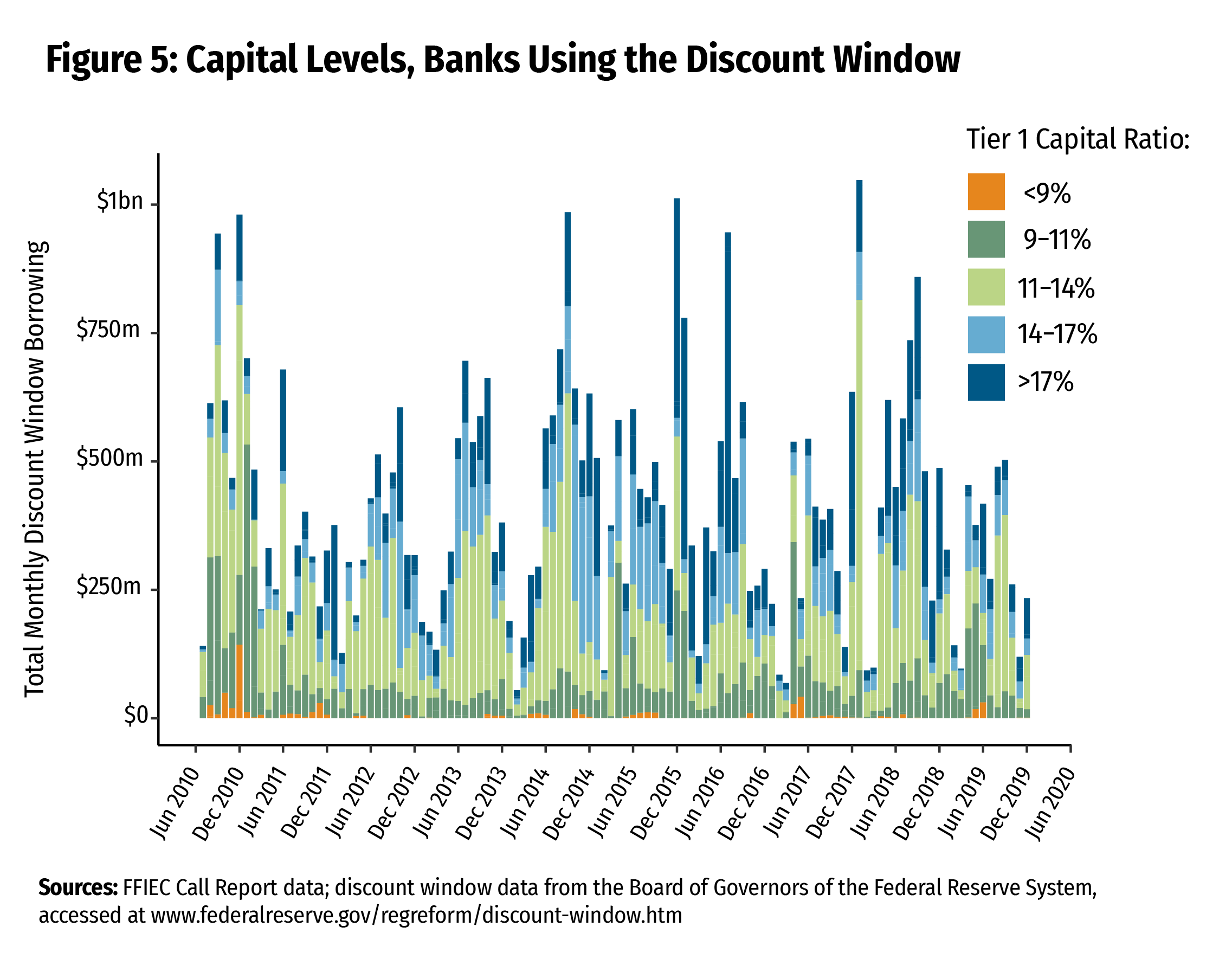

Discount window usage is published quarterly, on a two-year lag. We looked to see if the data align with the perception that banks in poor financial shape are heavy users of the facility. The results show a very different picture. In fact, stronger banks have comprised the majority of discount window borrowers over the past decade (see Figure 5).

Although setting up access to the discount window is free, it does require banks to take steps to open the borrowing line for at-the-ready access. Banks must fill out paperwork and pledge collateral. Testing is also critical to understand how borrowing works and to ensure that proper sign-off protocols are followed so that borrowing can be executed seamlessly when needed. For more information on how to set up access to the discount window, visit www.frbdiscountwindow.org.

Conclusion

Deposits have continued to evolve since the days of my first passbook savings account, and community banks remain a vital and important business model for the communities they serve. I hope that sharing information about these three risk areas that banks should plan for — deposit competition, deposit behavior, and on-the-ready contingent funding — provides community banks with additional tools to further their resiliency and vitality.

- 1 See FFIEC Call Report data.

- 2 See Faisal Islam, “Do Instagram and TikTok Mean Banks Are Less Safe?” BBC News, March 29, 2023, available at www.bbc.com/news/business-65107122.

- 3 Deposit betas are changes in deposit rates due to prevailing market rate changes.

- 4 See Emily Greenwald and Doug Gray, “Essentials of Effective Interest Rate Risk Measurement,” Community Banking Connections, Third Quarter 2013, available at www.cbcfrs.org/articles/2013/Q3/Essentials-of-Effective-Interest-Rate-Risk-Measurement.

- 5 See Emily Greenwald, Sam Schulhofer-Wohl, and Joshua Younger, “Deposit Convexity, Monetary Policy, and Financial Stability,” Federal Reserve Bank of Dallas Working Paper 2315, October 2023, available at www.dallasfed.org/-/media/documents/research/papers/2023/wp2315.pdf.

- 6 See the FDIC’s press release at www.fdic.gov/news/press-releases/2022/pr22075.html.

- 7 This effect also holds when we look at the number of deposit accounts per branch and when we look at the deposits of non-CBOs.

- 8 This was the total as of September 15, 2023, excluding credit unions.

- 9 See President Logan’s May 18, 2023, speech, “Remarks on Liquidity Provision and on the Economic Outlook and Monetary Policy,” at the Texas Bankers Association in San Antonio, available at www.dallasfed.org/news/speeches/logan/2023/lkl230518.

- 10 See Olivier Armantier, Helene Lee, and Asani Sarkar, “History of Discount Window Stigma,” Liberty Street Economics, available at https://libertystreeteconomics.newyorkfed.org/2015/08/history-of-discount-window-stigma.

- 11 See the press release from the Board of Governors of the Federal Reserve System, available at www.federalreserve.gov/boarddocs/press/monetary/2003/20030106/default.htm.